Core banking modernization rarely fails because a team cannot draw the future-state platform. It fails earlier, when system boundaries, ownership, cutover assumptions, and operating controls are still ambiguous but delivery has already committed to a path.

This is an architecture lens for teams working through core banking modernization, digital banking onboarding, retail and business banking integration, commercial lending systems, and business banking payments. The goal is not to add more diagrams. The goal is to force the decisions that reduce delivery risk before migration work hardens around weak assumptions.

Why modernization fails before the migration starts

Modernization pressure usually shows up around the core platform, but the real risk often sits in the surrounding systems: onboarding journeys, lending origination, payment streams, document workflows, CRM, fraud controls, reporting, notification services, and operational support queues. Each dependency can become a migration blocker if the architecture treats it as background plumbing.

The first warning sign is a plan that describes the target platform but does not say who owns customer state, account-opening status, payment status, lending handoffs, exception queues, data reconciliation, and rollback decisions. Without those decisions, teams may ship a technically modern system that is harder to operate than the system it replaced.

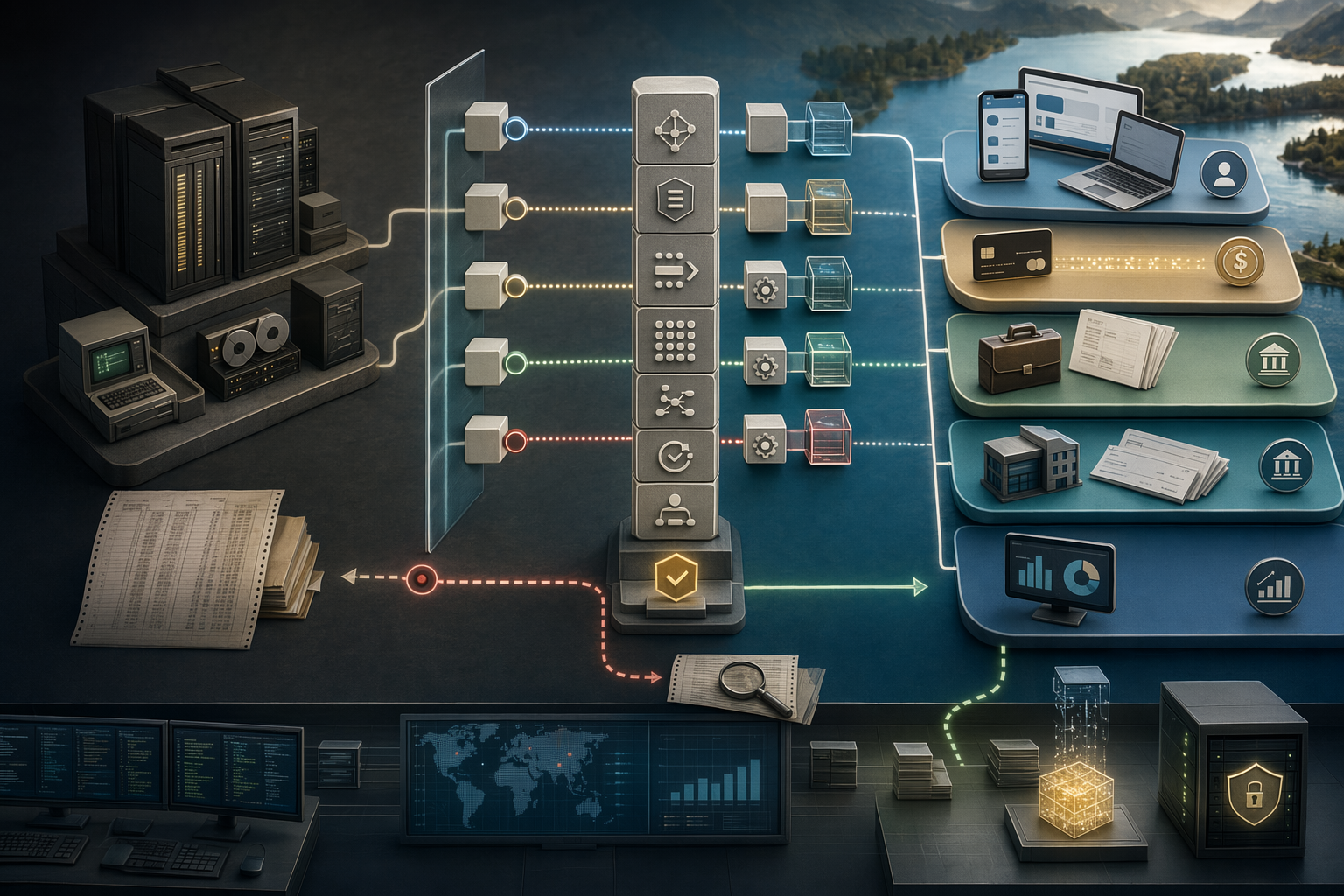

System-of-record boundaries

Core banking modernization needs explicit system-of-record boundaries. Customer, account, product, balance, lending, document, and payment records cannot all be informally owned by whichever system happens to update them first. The architecture should state where each record is mastered, which systems can propose changes, which systems can approve changes, and how downstream systems learn that a change is final.

This is where many banking programs need an integration boundary map rather than another application diagram. A useful boundary map shows the record owner, contract owner, event or API contract, retry behavior, reconciliation path, and operational owner. It also makes clear which dependencies are temporary migration scaffolding and which are part of the future operating model.

Digital onboarding and downstream dependency risk

Digital banking onboarding can look like a product workflow, but it depends on a chain of systems: identity verification, customer records, product eligibility, account opening, documents, funding, notifications, entitlements, and support. Retail and business banking onboarding become risky when the journey is treated as a single flow without clear failure states.

The architecture should identify where onboarding can pause, where it can retry, where human review is required, and where a customer or banker needs a reliable status. It should also show which downstream systems are allowed to receive provisional state and which systems should only receive confirmed state.

Integration contracts and exception handling

Integration contracts are control points in a modernization program. A contract should define the business event, required fields, source-of-truth reference, idempotency rule, retry expectation, versioning policy, error response, and ownership path for exceptions.

For integration-heavy banking environments, the sync-versus-async decision matters. Some checks need immediate response, such as eligibility, validation, or authorization. Other work is safer as an event, queue, or workflow step where retries, partial completion, and exception handling are visible. A contract that does not describe failure behavior is not ready for migration.

Commercial lending and payment-stream impacts

Commercial lending systems and business banking payments raise the stakes because they often carry downstream impact, operational exceptions, audit expectations, and time-sensitive status changes. Lending workflows may depend on approvals, collateral, documents, product setup, account linkage, and servicing handoffs. Payment streams may involve authorization, limits, message mapping, settlement timing, downstream notifications, reconciliation, and exception operations.

Modernization plans should make these impacts visible before cutover. Teams need to know how transaction references move across systems, how duplicate or delayed messages are handled, where operational exceptions land, and which owner is accountable for correction. This is where a risk register and owner/action list are more useful than broad modernization language.

Cutover, rollback, and reconciliation

Cutover is an architecture concern, not just a release plan. Before migration starts, teams should know which functions can move in waves, which interfaces need temporary compatibility, which datasets require reconciliation, and which rollback paths remain realistic after records begin moving through the new model.

A credible rollback and reconciliation checklist should cover parallel-run assumptions, validation checkpoints, payment and account-state comparisons, exception thresholds, business approval gates, support ownership, and the decision tree for rollback or forward-fix. The checklist should also name what cannot be rolled back cleanly, because those points require stronger readiness evidence before release.

What an architecture decision memo should force

An architecture decision memo should make the decision clear enough for executives, architects, delivery leads, product owners, and operational teams to act on. It should not be a slide deck that hides unresolved tradeoffs.

For a core banking modernization decision, the memo should force these artifacts into the open: the decision needed, options compared, system-of-record boundaries, integration boundary map, delivery and operating risks, risk register, cutover and rollback assumptions, reconciliation model, owner/action list, and recommended path. It should also identify which unknowns must be resolved before vendor commitment, migration sequencing, or funding decisions become difficult to reverse.

What to prepare before a review

A short architecture review is more useful when the real constraints are visible. Before a review, gather the current architecture sketch, integration inventory, onboarding or servicing flow, core and downstream system list, known incidents or failure modes, migration roadmap, vendor/platform constraints, data reconciliation concerns, and the decision that needs to be made.

The review should clarify which systems and teams are affected, where the main failure modes sit, what information is missing, whether a short decision sprint is enough, and which artifact is needed next: a decision memo, risk register, integration boundary map, rollback/reconciliation checklist, or owner/action list.

Next step

If your team is preparing a core banking modernization, digital banking onboarding change, commercial lending system integration, or business banking payments modernization, start by making the architecture decision explicit before migration assumptions become expensive.

Related resources: Core Banking & Digital Banking Architecture Review, Architecture Review Checklist, and Architecture Advisory.

Need this reviewed in a real modernization program?

Book architecture review Review core banking architecture support

Join the discussion

You must be logged in to post a comment.